On this Expert Insight Series, we interview Sean Edmonson of Tecum Capital Partners. Since 2006, Tecum has invested close to $1B across the middle-market. Tecum focuses primarily on backing founder- and entrepreneur-owned businesses with strong leadership, operating in manufacturing, business service, and distribution sectors.

Sean oversees fund investment activities including deal execution and negotiation, due diligence, debt finance negotiations, and portfolio support and value creation. Before Tecum, Sean worked in commercial and industrial investment banking, gaining experience in strategic advisory, sell- and buy-side advisory, and raising capital. Sean currently sits on several boards including BP Express, Connecticut Electric, FSC Lighting, National Power, and F&S Tool.

In this series installment, Sean shares how Tecum has used the power of data in their portfolio companies to become a top performing fund in their category.

Watch the full interview, listen to the podcast episode, or read the highlights below.

Top 4 Takeaways:

- Dashboards and KPIs help align private equity firms and their portfolio executives on the value creation plan, which empowers leadership and drives accountability.

- There are several ways lower middle-market companies stand to benefit from proactive investment in BI.

- Data differentiates portfolio companies through higher valuation and faster exits.

- “Tread cautiously, actively invest” – an economist’s advice for private equity firms in the current economic headwinds.

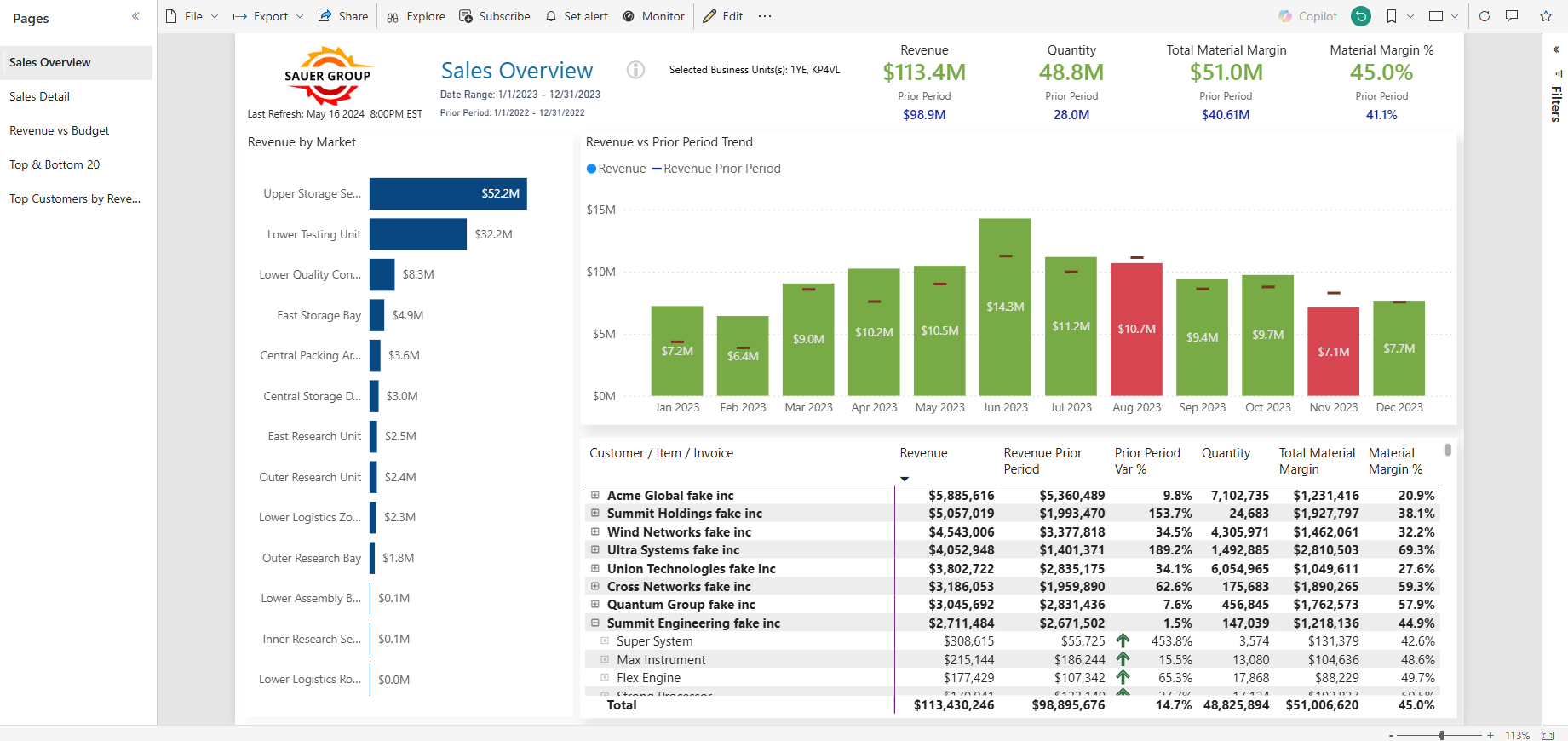

How Private Equity Uses Dashboards and KPIs to Empower Portfolio Companies and Drive Accountability

“Empowerment comes down to alignment early on.” – Sean Edmonson

Generally, many of Tecum’s investments require process changes in order to create value. As a best practice, Tecum aligns early with company leaders to co-define the pillars of their value creation plan. They then work backward to identify the process steps and the performance metrics needed to create accountability and increase value over the holding period. These efforts lead to dashboards that empower management teams to advance the plan rather than spending time digging for data and producing reports.

This process creates what Sean calls a culture of empowerment. He adds, “Folks don’t want to be handcuffed or told by higher ups what to do. They like having a culture of accountability and understanding what winning looks like.”

Using Data in the Lower Middle-Market Investment Landscape

“At the heart of many of our success stories, is a central focus around data to drive decision making and accountability within the organization… they have reliable data to make good decisions, and they use it to drive their work.” – Sean Edmonson

Because high-performing employees like to see the score and have insight into their performance, the most successful manufacturing and services companies provide real-time (or at least daily) visibility into the KPIs most important to each employee’s. Sean says, “I’m a huge believer in radical transparency. And I would say with some of our best run organizations – especially where I’ve seen it come to life – is in manufacturing organizations. It’s a very complex operating environment. Given tolerances, throughput, and some of the dynamics that go into world class shops, those folks like to be measured, and they like to know what winning looks like on a given day.” Additionally, “In our best run services companies, service technicians have really strong visibility into production goals in a given week. And they know when they’re up or down as they work towards that weekly target.”

Chuck Coonradt, in his bestselling business book, The Game of Work, asks, “If winning isn’t important, why do we spend all that money on scoreboards?” With this in mind, investors should increase BI investment throughout manufacturing organizations to increase job ownership and encourage achievement.

Data Increases the Valuation of Manufacturing Companies

A primary consideration for Tecum when assessing valuation during due diligence is data. They seek to understand a company’s accessibility to and grasp on the numbers. To what extent is the management team able to rely on data to inform decisions and strategy?

“If you don’t have any type of dashboarding or KPI system, it’s a major deduction on the value of your company if you’re looking to sell to institutional investors as a platform.” – Sean Edmonson

When evaluating a company’s readiness to grow and increase in value, a primary hurdle is weak or underdeveloped systems for automating data intelligence. Non-data driven companies require a cultural shift, process refinement, and technology integrations that can take months or years. By contrast, companies with the greatest potential already have a system for organizing and surfacing their data. According to Sean, “If you have data that gives you 70% of the picture, helping you to instinctively make good decisions, you are ten steps ahead of the rest of the market.”

An Economist’s Advice for Private Equity Firms

An economist who recently advised Tecum on the current economic headwinds advised, “Tread Cautiously, Invest Actively.” Tecum does this by watching the consumer environment, over-equitizing new deals, and performing tiered scenario planning. They invest actively in durable industries and companies with strong employee bases and highly skilled workers.

In this hawkish market, a defensive stance feels natural, but leaders must face the facts that a purely contractionary response leads to median company performance (Birshan et al, 2022). Similarly, Blue Margin recommends that companies adopt an offensive, expansionary stance (informed by data) during economic challenges. History favors the brave.

More on Tecum Capital

Tecum means with you in Latin. This branding guides Tecum in how they build partnerships, focused on establishing trust and strong relationships with founders. They’ve been investing in the lower middle-market for 17 years and have resisted the temptation to go up-market. For Tecum, great people, passion, and strong character matter more than the size of the company.

As Sean puts it, “We’re really passionate about helping these folks go out and win and succeed. And a lot of them care about their legacy. A lot of them care about their people. And they want to know that when they look across the table at someone, it’s more than dollars and cents. It’s always a really honest approach… it’s being good people and working hard.”

Tecum also prioritizes process improvement, documentation, and execution. They identify constraints early on in the investment, then they look to equip portfolio executives to advance their companies and capitalize on investments in technology, equipment, and people.

If you’d like to connect with Sean, do so via LinkedIn or the Tecum team page. Tecum Capital can be reached here: Tecum Capital

If you’d like to explore how Blue Margin’s team can help you use data visibility to drive growth and inform decision making, contact us below.